CLO managers are facing the worst new-issue economics in years, with BSL new-issue volume down 21% year over year. Thin leveraged loan supply, compressed spreads and high liability costs are keeping day one equity returns deep in the red, but the market is deploying a suite of countermoves to keep deals crossing the line. Captive CLO equity continues to drive most issuance, but as managers get creative third-party equity investors are starting to find opportunities.

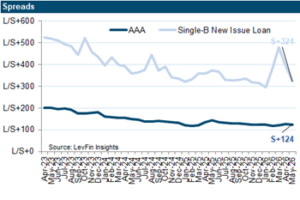

CLO Triple A spreads continue to edge down and are pricing at an average of 121bps currently, according to LFI data. But as leveraged loan spreads are also compressing modeled equity returns remain stuck in the low-double-digit IRR range, according to sources. CLO equity returned negative 10% for day one arb and 11% IRR year to date through mid-May, according to BofA Global Research, which gives investors significant pause on new commitments.

“Equity has often been the limiter for growth of the CLO market; it’s now about access to loans,” explained Alex Danehy, head of US CLOs at Deutsche Bank. “The asset class can’t continue to print record issuance numbers over the long term, which would ultimately result in underperformance.”

Countermoves

Captive CLO equity continues to dominate the market, but investors are finding opportunities deal by deal. To attract first loss buyers, managers can pull several levers, said sources. The most common is a side letter that redirects roughly 5bps to 10bps of the management fee to the equity investor. Another option is a fee holiday, where the manager waives fees from closing to the first payment date. Those savings flow directly into the first equity distribution, the most important for IRR calculations.

Some managers also offer first payment guarantees, effectively collateralizing support against their fees to ensure a minimum initial payout. “The amounts stay modest, but the gesture shows alignment,” said a buysider.

While not purely a countermove, a handful of print-and-sprint CLOs pop up once in a blue moon, and this can result in a windfall for a manager and investors. In March, after the Iran war started, loans traded off roughly a dollar, a handful of attractive print-and-sprint deals emerged from opportunistic managers. Those managers with empty warehouses took advantage and built par, which made the deals more compelling for third-party equity buyers.

12% is the new 15%

The other thing the market is doing to keep deal flow going is recalibrating return expectations. Where equity buyers once demanded 15%-plus IRRs, sources say 11%-13% is now the more common range, given the challenging spread compression on the asset side. With portfolio spreads around 300bps or tighter, it is said to be very hard to think about generating returns north of 15%. “As long as LPs are aware that this is the new regime of spread targets, then the CLO equity machine will continue,” said a banker. “Marketing has become more realistic in this cycle, reflecting that credit is at historic tights across the spectrum.”

While 12% may be the new target, even that reduced level is a push for many managers. A CLO executive explained that getting low-double-digit returns largely depends on manager tier and negotiations: “It really depends on the assumptions used, but equity returns are hard to push into double digits at current creation prices with a mostly secondary ramped de novo portfolio and a low tier-two or less liquid shelf WACC, though low teens returns remain achievable with current tier-one WACC, favorable portfolio costs, resets and subsidies.”

The situation does seem to be improving. According to one banker, recent Triple A tightening has helped pushed modeled returns toward 13.5% in mid-May in some cases, a swing from below 10% just at the start of the month. That could reopen the market to sidelined equity buyers, although some LP buyers, such as pensions and endowments, are said to remain active.

One large CLO ETF fund sees a potential bull case for large, liquid Triple As tightening to 110bps (a level last seen in February 2025) as lower issuance compresses spreads, a floor that could materially improve equity profiles. Other CLO executives say Triple As need to compress even further to the low 100s to significantly motivate third party equity buyers.

Retail capital hunt

CLO equity fundraising is also moving cautiously toward a more balanced mix of institutional and retail demand. Interval funds mixing equity and junior mezz are emerging as the vehicle of choice for that, though most stay small and do not yet drive the market independently, said sources. The open question is whether retail investors will tolerate the liquidity constraints that come with these products, particularly after negative headlines around BDCs. How private credit funds handles that issue will shape the next phase for CLOs also. One skeptic for retail as an outlet for CLO equity said the 10-20 points performance variance between CLO managers makes locked in capital extremely difficult for the asset class, as opposed to a diversified strategy with small positions.

Multiple managers are building interval funds now. Early this month, MetLife’s PineBridge launched an interval fund targeting retail CLO equity demand, joining VanEck in a push to broaden its investor base beyond institutional allocators. The VanEck CLO Opportunities Fund (CLOIX) is an actively managed CLO investment strategy that invests primarily in equity and junior mezzanine tranches of CLOs of BSLs. “There is interest in interval funds and private wealth distribution as additional sources of demand for CLO equity and related products,” said a CLO tranche trader.

Minority stakes

One dealer reported that half its pipeline involves third-party equity as minority investors. Captive vehicles only need to buy 51% themselves, so they look to place the rest elsewhere, sources said. A few buyers take majority pieces in new-issue deals, but that remains the exception. Roughly one buyer is visible to do true primary majority equity pieces, sources said. Managers have a long-term reason to accommodate outside capital. If they eventually need liquidity on a control position inside a captive vehicle, it helps to have investors who already know the platform and the portfolios. That depth supports future growth.

For control equity, tranche investors say the math doesn’t work, e.g., Triple As would need to reach low 100s to attract interest, said one credit hedge fund CLO tranche trader.

Discerning captive equity

Captive CLO equity continues to support the majority of new deals, but the volume is slowing, said sources. Bain and CVC renewed their captive programs, yet several small and midsize platforms are struggling. One deal lawyer noted some $300mn-$400mn captive raises have seen “diminished” LP interest. “No investor wants to reward low performance,” said sources. “Size matters — large platforms have the advantage of substantial workout teams.”

Performance will determine whether investors back a second fund. Some managers have navigated the environment well; e.g., maybe they missed First Brands but handled software well. Others landed on the wrong side of both those issues and now underperform. That sentiment also holds true for deep-pocketed parents: “No parent company keeps putting good money after bad indefinitely,” sources said.

Many of these captive equity funds carry four-year lives and are sitting roughly two and a half years in, so time remains. But eventually, if follow-on support fades, overall issuance will slow sharply as these unnatural buyers disappear, unless the arbitrage improves, or structures change enough to produce returns that work for third-party equity.

Given the headwinds for captive equity fundraising, cross-platform partnerships are emerging as another important source of equity support to grow a CLO business, said sources. Equity partnerships can help managers address “exit velocity,” which is a challenge, particularly for newer managers that are running out of initial investment funds.

Looking ahead

Investors and bankers expect the modest thaw in May to continue into June, but issuance is likely to remain below trend absent a surge in M&A-driven loan supply or rate cuts. Still, hope remains. The market appears spring-loaded: Natural cash buyers — pensions, endowments, and non-life insurers — continue growing CLO exposure and reviewing deals closely, positioning the market for a snap-back if the arbitrage normalizes.

David Graubard

david.graubard@levfininsights.com

+1 646 361 6095