Investor sentiment toward private credit has softened in recent months after a prolonged period of strong growth and capital inflows. A combination of macro uncertainty, sector-specific concerns, and negative headlines has prompted lenders and investors to take a more cautious stance.

Several factors are contributing to this shift, including:

- Potential disruptions to software borrowers and other sectors with meaningful AI exposure

- Negative press surrounding Blue Owl and broader questions about liquidity dynamics in private credit vehicles

- Concerns that rapid fundraising over recent years may have weakened underwriting discipline in parts of the market

- Broader worries that a slowing economic backdrop could push default rates higher

Periods like this are not unusual in credit cycles. Market confidence can change quickly, particularly when headline events create uncertainty around relatively opaque asset classes. We saw a similar dynamic last summer following the “gradually-then-suddenly” bankruptcy filings of Tricolor and First Brands, which temporarily rattled investor confidence across segments of the private credit ecosystem. In fact, in the four-decade history of the modern leveraged finance market there have been three significant default spikes: early 1990s when the original junk bond frenzy fizzled in the aftermath of the 1991 recession, the early 2000s when the combination of the dot-com bubble bursting and the terror attacks of September plunged the economy into recession and the Great Financial Crisis of 2008/2009. But, to paraphrase Nobel Prize winning economist Paul Samuelson’s famous quip, the market has called no fewer than seven more default spikes that failed to materialize since 1990 including (1) irrational exuberance of 1996, (2) Russian debt default/Long–Term Capital implosion of 1998, (3) Government shutdown/US Credit Rating downgrade of 2011, (4) retail-pocalyse of 2014, (5) oil price crash of 2015, (6) rate tightening cycle of 2018, (7) Covid-19 cessation of 2020, and (8) Ukraine war/inflation spike of 2022-2023.

How the current environment evolves will depend on a range of macro factors — including economic growth, interest rates, and broader credit market conditions — that are impossible to predict. In response, many private credit managers are actively re-underwriting portfolios, particularly in sectors such as software where technological disruption is a growing consideration. An important part of that process involves placing documentation strength and covenant protections under closer scrutiny. One area where this question becomes particularly relevant is covenant quality.

Private Credit vs. Syndicated Markets: Structural Differences Still Matter

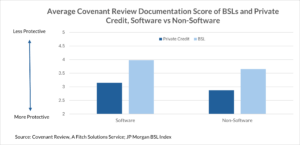

On average, private credit documentation remains more protective than broadly syndicated loan (BSL) markets. Direct lenders typically negotiate within smaller lender groups, allowing for tighter controls and more customized protections.

Two structural areas highlight this distinction:

Baskets

Private credit software baskets are, on average, materially tighter than those observed in the syndicated market. For example, the average debt issuance limit for private credit software borrowers stands at approximately 1.6x pro forma EBITDA — roughly half the 3.2x levels commonly seen in syndicated transactions.

Loopholes

Structural loopholes, such as the well-known “J.Crew” intellectual property transfer provision, appear far less frequently in private credit documentation. Our data shows this provision present in only about 2% of private credit software loans versus roughly 23% in the syndicated market.

These differences are not academic. They translate directly into lender leverage during stress scenarios, recovery outcomes, and ultimately investor returns.

The Real Story: Dispersion Is Growing

Averages only tell part of the story, however.

As capital flows into private credit accelerated in recent years, competitive pressures increased. Sponsors are negotiated for greater flexibility, new lenders are entering the market, and documentation quality is showing greater dispersion between the strongest and weakest deals.

In other words, private credit may still be more protective on average — but not uniformly so.

This dispersion is likely a more important structural development than any individual headline around liquidity or loan pricing. For allocators and lenders, understanding which deals maintain strong protections — and which do not — is becoming a critical differentiator.

Perception vs. Reality in the Current Market Cycle

Historically, documentation strength—along with collateral coverage—has exerted a major influence on lender outcomes in distressed and bankruptcy situations.

That is why covenant analysis remains central to evaluating risk in both private and syndicated credit markets.

Why Data Matters More Now

As the asset class scales, anecdotal comparisons and manager marketing claims are no longer sufficient.

Independent covenant intelligence — including tools such as Covenant Review and the broader CreditSights analytical platform — enables investors to move toward data-driven risk assessment.

By systematically comparing documentation across deals, sectors, and time periods, market participants can:

- Benchmark underwriting discipline

- Identify emerging documentation trends

- Evaluate downside protections before stress occurs

- Distinguish structural strength from marketing narratives

In an environment where capital is abundant but protections are uneven, information asymmetry creates both opportunity and risk.

That is where rigorous covenant protections — and the insight provided by CreditSights — can provide lenders an edge in girding their portfolios against volatile times and potential increase in default rates.

To gain deeper visibility into documentation strength and deal dispersion, request a trial of CreditSights and explore the full platform.