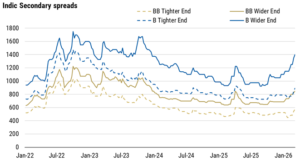

Sub-investment grade tranches of European CLOs have widened in secondary to levels last seen during the spread blow-out that followed April 2025’s Liberation Day.

Average secondary spreads for Single B tranches topped 1000bps DM at the close of last week, and Double Bs approached 700bps DM, per Houlihan Lokey’s CLO spread indices, which track the most liquid bonds in each rating group.

Behind these averages is a significant dispersion between individual deals, which has reached record levels at the bottom of the stack.

Ranges currently span 950-1250bps for deals without distressed Market Value OCs (MVOCs), but go all the way out to 1400bps for deals under more significant pressure, or trade solely on cash prices, say sources.

The MVOC measures the cushion of collateral value available to support debt tranches, should a deal be liquidated.

Trading on MVOC

Much of the deal-level dispersion in Single B tranches stems from portfolio exposures to software companies, whose loan prices have slumped this year on fears of AI disruption.

CLO portfolio allocations to software vary significantly by manager, from close to zero to the high teens, with an average of approximately 7% in Europe.

“CLO portfolios with software exposure at the upper end of the range face greater pressure on their MVOC ratios, which directly impacts tranche pricing in secondary,” said Rondeep Barua, portfolio manager in the Alternative Credit team at Ninety One. “Depending on how a manager has navigated other recent market events, some deals may also be subject to a manager-specific premium.”

CLO managers across Europe have taken differing approaches to AI disruption risk and software. A panelist at this week’s FT Live CLO conference in London commented that some managers opted to “sell first and ask questions later”. Others say they have selectively added exposure to discounted names that they think were oversold.

Other challenged sectors, such as chemicals, plus idiosyncratic problem credits such as First Brands, have further weakened market MVOC levels in late 2025 and early 2026. The emerging energy crisis stemming from the Middle East war is adding another layer of uncertainty.

As a result, an increasing number of CLO Single Bs are now heading into negative MVOC territory. Recent BofA research indicates that approximately 15% of European CLOs now have negative MVOCs, up from 3% in January and almost none in 2025. A “handful” of Euro CLO Double B tranches also have MVOC ratios below 100%.

While a negative MVOC increases that tranche’s price volatility – and even tradeability – it does not indicate an imminent loss for bondholders. Loan prices can recover, and CLO structures contain various cash trap mechanisms designed to protect bondholders.

On this point, the technology segment of the JP Morgan European Leveraged Loan Index has lost 4.86% year-to-date – but so far in March it has gained 1.49% in a partial retracing of its steps.

IG more resilient

Unlike the post-Liberation Day response – in which all tranches across the CLO capital structure widened in a knee-jerk reaction to broad market shock – the latest repricing of risk has been more concentrated in CLOs’ lowest rated tranches.

Triple As, for example, have widened to ~108bps DM on average, compared with wides of ~142bps in April 2025, according to Houlihan Lokey data, while Triple Bs have moved to ~315bps DM now versus 395bps last April.

Anna Carlisle

anna.carlisle@levfininsights.com

+44 (0)20 7469 0981